- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- Монгол хэл

April 2026 ECB Preview: Waiting For More Information

Summary

- On Hold: The ECB will stand pat at the April meeting, awaiting further data on the impact of conflict in the Middle East on the eurozone economy

- Guidance Unchanged: Policymakers should reiterate that a 'data-dependent' and 'meeting-by-meeting' approach will continue to be adopted moving forwards

- Scenarios In Focus: Whether the economy is evolving closer to the 'baseline' or the 'adverse' scenario will be key to the policy outlook, though explicit guidance on the prospect of policy tightening in June is likely to be avoided

Policy On Hold

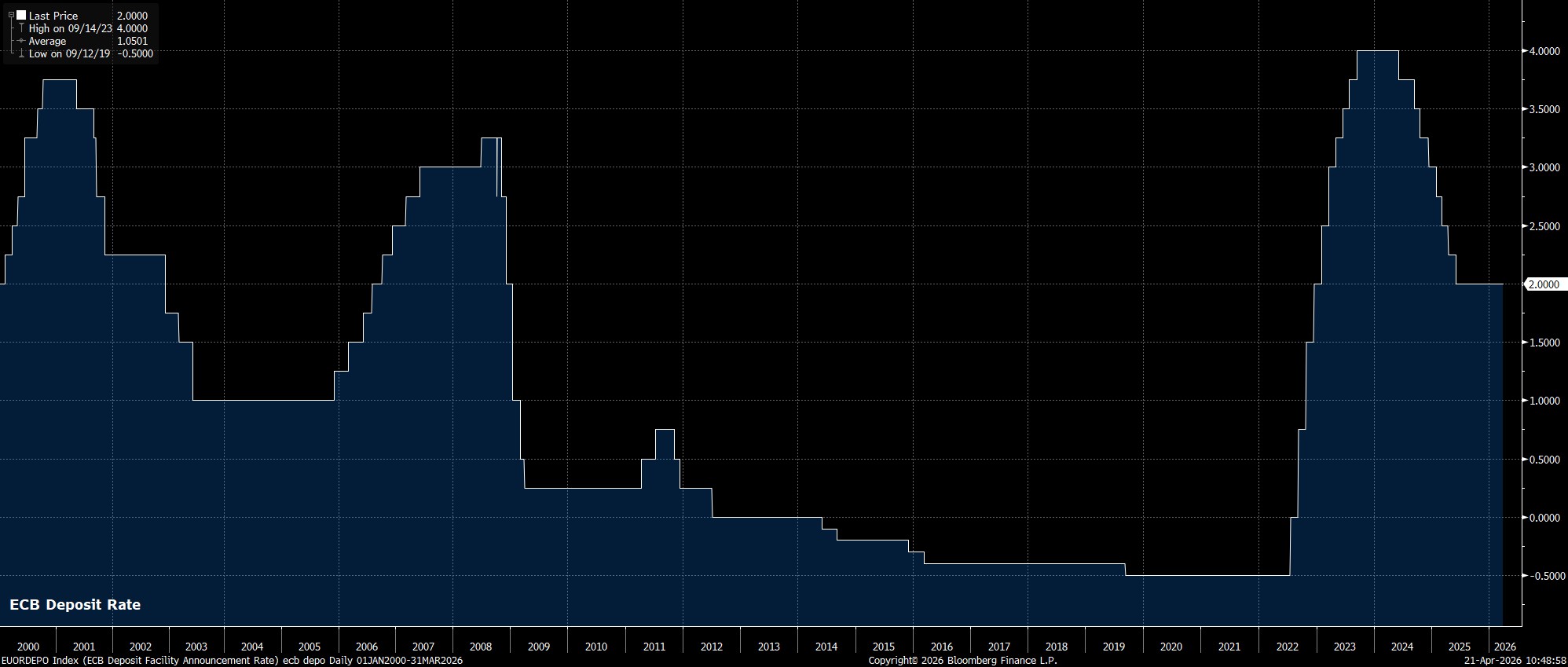

As noted, the Governing Council are set to maintain all policy settings at the conclusion of the April confab. Consequently, the deposit rate should be held steady at 2.00%, the level at which it has stood since the easing cycle concluded last summer, with money markets pricing just a 10% chance of a 25bp hike this time around.

Swaps do, though, discount a relatively swift path of policy tightening over the remainder of the year, with a 25bp increase fully discounted by the July meeting, and another such hike essentially fully discounted by the end of the year.

While the policy decision itself is unlikely to bring much by way of surprise, the degree of any disagreement among GC members will provide some intrigue. Though the ECB don’t publish a formal voting record, President Lagarde’s comments on this front at the post-meeting press conference, as well as any ‘sources’ reports, will bear watching closely, especially with the likes of Nagel, Wunsch, Kazimir, Muller, and Sleijpen having openly touted the prospect of policy tightening in recent weeks.

Guidance To Be Repeated

Turning to the accompanying policy statement, the Governing Council will likely repeat the policy guidance with which market participants have now become incredibly familiar. Namely, that a ‘data-dependent’ and ‘meeting-by-meeting’ approach will continue to be followed, and that no ‘pre-commitment’ is being made to a particular policy path.

On the geopolitical situation, in particular, again a repetition of the lines used in March is likely, with the overall policy stance remaining ‘well positioned’ to navigate the impact of conflict in the Middle East, and that policy will continue to be set ‘as appropriate’. While policymakers could include a nod to potential rate hikes in the statement, doing so seems relatively unlikely, given that the Governing Council are unlikely to want to box themselves in to a particular policy path, particularly with six weeks until the next meeting in June, and the economic outlook remaining highly fluid.

Scenarios Hold The Key Moving Forwards

At the March policy meeting, in light of the fluidity of the current backdrop, the ECB published not only the usual set of staff macroeconomic projections, but also two additional scenarios – one ‘adverse’, and one ‘severe’ – to reflect a range of potential ways in which the impact of the surge in energy prices may manifest itself.

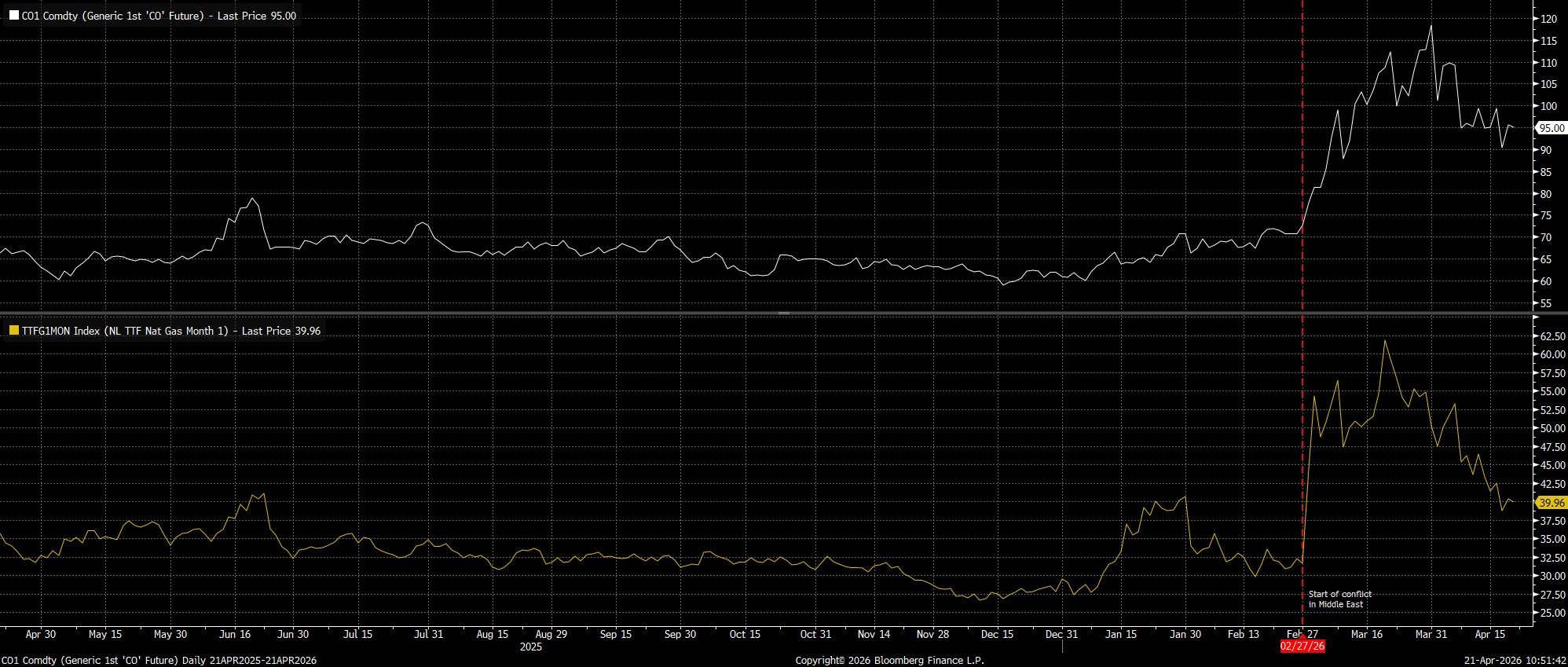

At the time of writing, it currently appears that the eurozone economy is sat somewhere between the ‘baseline’, and the ‘adverse’ scenario outlined around a month ago. Of course, the primary determinant of which scenario is being followed is energy prices. Currently, front Brent futures trade around $95bbl, having fallen around 15% since the March meeting, with the December future around $81bbl; meanwhile, TTF futures sit around the €40 mark from the front month (May), out to December 2026. All told, and taking into account the significant surge seen in both front contracts at the tail end of last month which has since retraced, this probably leaves the eurozone economy somewhere between the ‘baseline’ and the ‘adverse’ scenarios. This chimes with President Lagarde’s assessment, with Lagarde having recently noted that the ECB is ‘not yet’ in the adverse scenario.

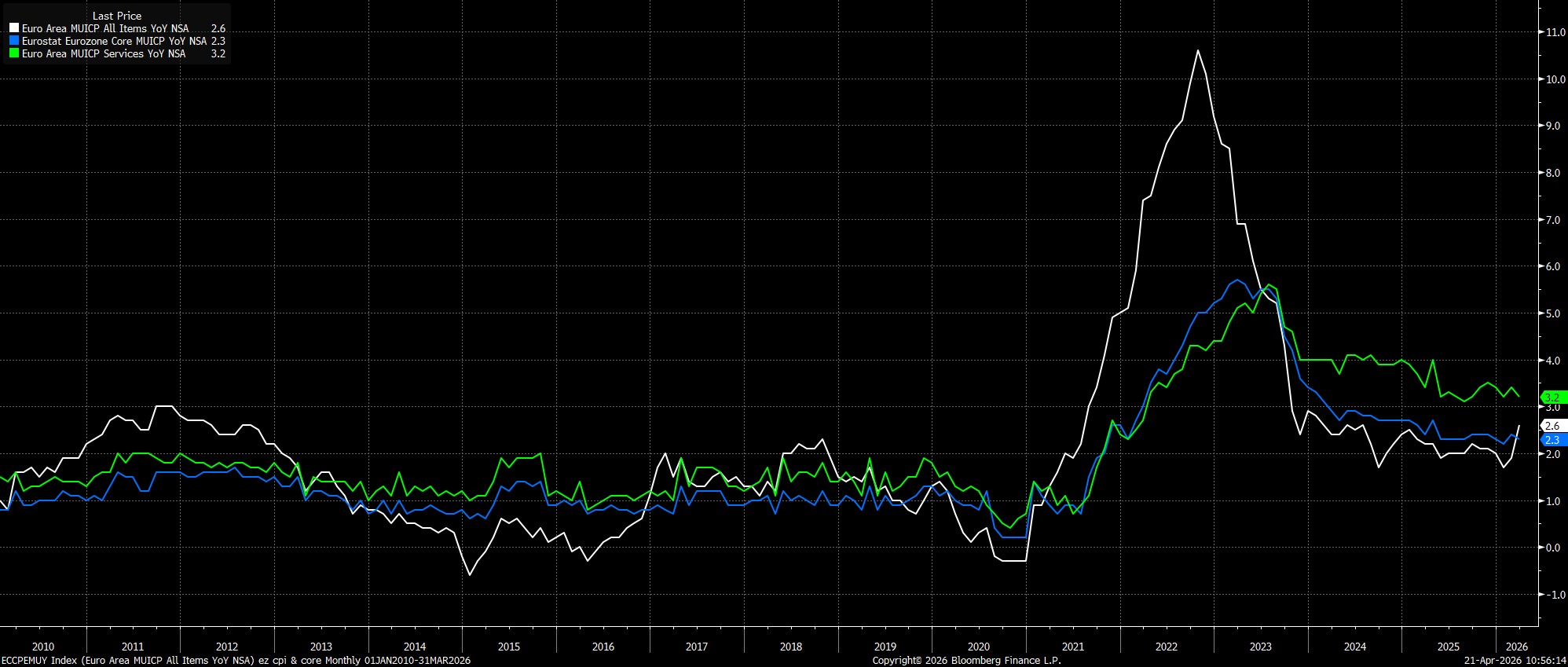

That said, the impact of higher energy prices has already begun to show up in headline inflation, with HICP having risen 2.6% YoY in March, up from 1.9% YoY in February, and the fastest annual pace since July 2024. Still, policymakers may seek some solace in both core and services inflation having dipped a touch last month, implying that price pressures are not yet broadening out across other areas of the economy.

Risk Of Persistent Price Pressures Remains Low

In fact, the risk of price pressures broadening out, and thus becoming somewhat more persistent, still seems relatively low at the current juncture.

Given the relatively anaemic pace of economic growth seen in the eurozone, and with risks to growth tilting clearly to the downside, corporates clearly have limited pricing power at this stage. Added to which, employees possess little by way of negotiating power in terms of earnings, given the somewhat loose labour market, in turn lessening the risks of a wage-price spiral developing, as was seen in the aftermath of the most recent energy shock in 2022.

Furthermore, inflation expectations remain well-anchored, further lessening the probability that so-called ‘second-round’ effects emerge, and also lessening the need for tighter policy in response to recent developments.

All that said, there is a risk that the ECB are minded to tighten policy anyway. The ‘baseline’ projections outlined last month pointed to headline CPI rising to 2.6% this year, before falling back to the 2.0% target in the following two years, though this was conditioned on market pricing at the time, which implied around 45bp of tightening being delivered over the course of the year, roughly the path that markets price at present.

A relatively rudimentary model suggests that the ECB failing to deliver the tightening that was assumed in the aforementioned projection would have little-to-no impact at all on where HICP peaks this year, and would have only a very marginal impact (around 3bp) on headline inflation next year. Importantly, standing pat in the present ‘neutral’ stance would cushion the impact of the ongoing negative demand shock on GDP growth, and the economy at large. Regardless, it seems increasingly likely that the debate around whether any policy tightening is required is one that’s likely to take place at the June meeting, in conjunction with the production of updated economic forecasts.

Lagarde To Give Little Away

President Lagarde will probably hint at this approach at the post-meeting press conference, having recently noted that policymakers require ‘more information’ before drawing conclusions on the policy outlook.

Besides that, Lagarde is likely to reiterate that inflation risks tilt to the upside, and that growth risks tilt to the downside, even if the economic outlook at large is still ‘deeply uncertain’. Any comments on Lagarde’s future, and whether she plans to see out her ECB term, ending in October 2027, are unlikely, with speculation regarding a potential early departure having quietened in recent weeks.

Conclusion

On the whole, the April meeting will be something of a ‘placeholder’ for the ECB, as policymakers continue to adopt a ‘wait and see’ approach, seeking additional clarity on how the economic outlook is likely to evolve.

Though the Governing Council seem to have inched closer to policy tightening in recent weeks, my view remains that doing so would represent a policy mistake, serving only to amplify the negative demand shock triggered by higher energy costs, which by their very nature will have a ‘temporary’ impact on headline inflation metrics.

With the caveat that plenty could change between now, and the June Governing Council meeting, further progress towards an end to hostilities in the Middle East, as well as signs of commodity flows beginning to normalise, should give policymakers the requisite confidence to stand pat once more next time out, with inflation expectations also likely to remain well-anchored.

The base case, hence, is that the ECB remain on hold for the foreseeable future, looking through a near-term ‘hump’ in HICP, and avoiding the temptation to commit a third policy mistake in the central bank’s relatively short history.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.